Insights

Real estate investing trends, strategies, and lending insights from LendingOne.

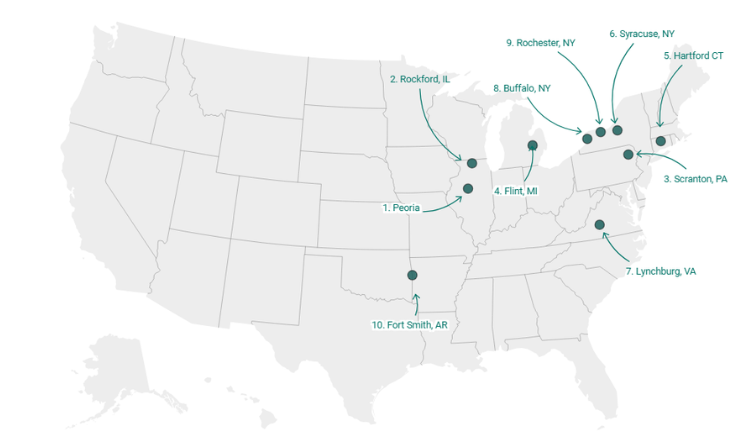

Top 10 Markets for Fix and Flippers in 2026

February 16, 2026

Real estate investing trends, strategies, and lending insights from LendingOne.

February 16, 2026